The Best 3-Card Credit Card Setups for 2026

The top 3-card wallet combinations for strong rewards across all spending categories. Amex, Chase, and mixed trifectas compared.

You do not need a dozen credit cards to have a good wallet. Three well-chosen cards can cover every major spending category at a strong earn rate, keep your annual fees reasonable, and simplify the mental overhead of “which card do I use here?”

The trick is choosing three cards that complement each other instead of overlapping. Here are three proven setups for 2026: the Amex Trifecta, the Chase Trifecta, and a Mixed setup that pulls the best from multiple issuers.

TL;DR

- Amex Trifecta: Best for travelers who value transfer partners and premium perks. Highest total credits but highest total fee ($1,220).

- Chase Trifecta: Best for flexibility and Visa acceptance. Reserve anchor fee is $795, with a simple $300 travel credit plus many other credits if you want them.

- Mixed Setup: Best for people who want to cherry-pick the strongest card from each issuer. More complexity, potentially the highest net value.

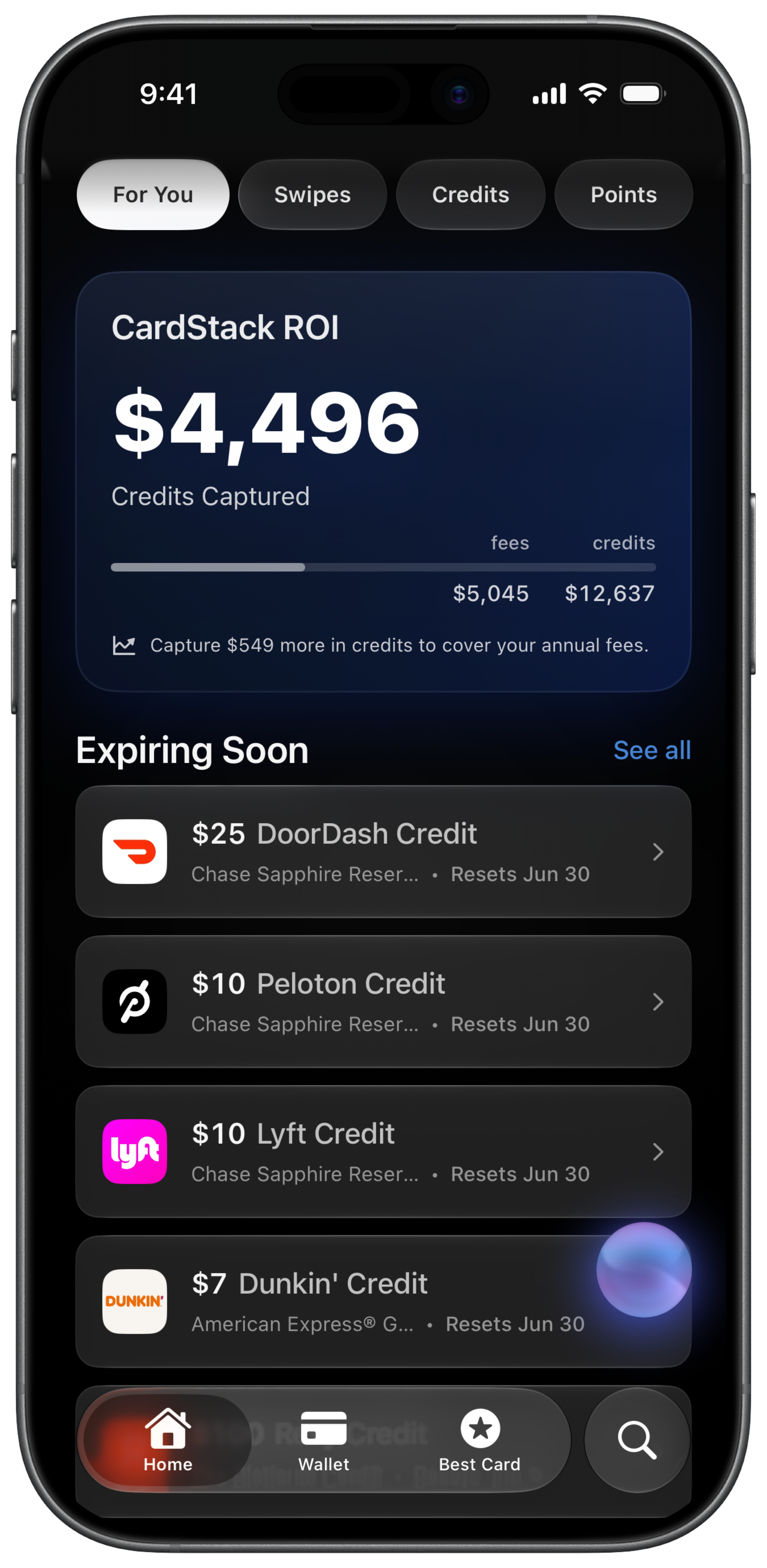

- Use CardStack to see exactly which card to pull at any merchant across your entire wallet.

Setup 1: The Amex Trifecta

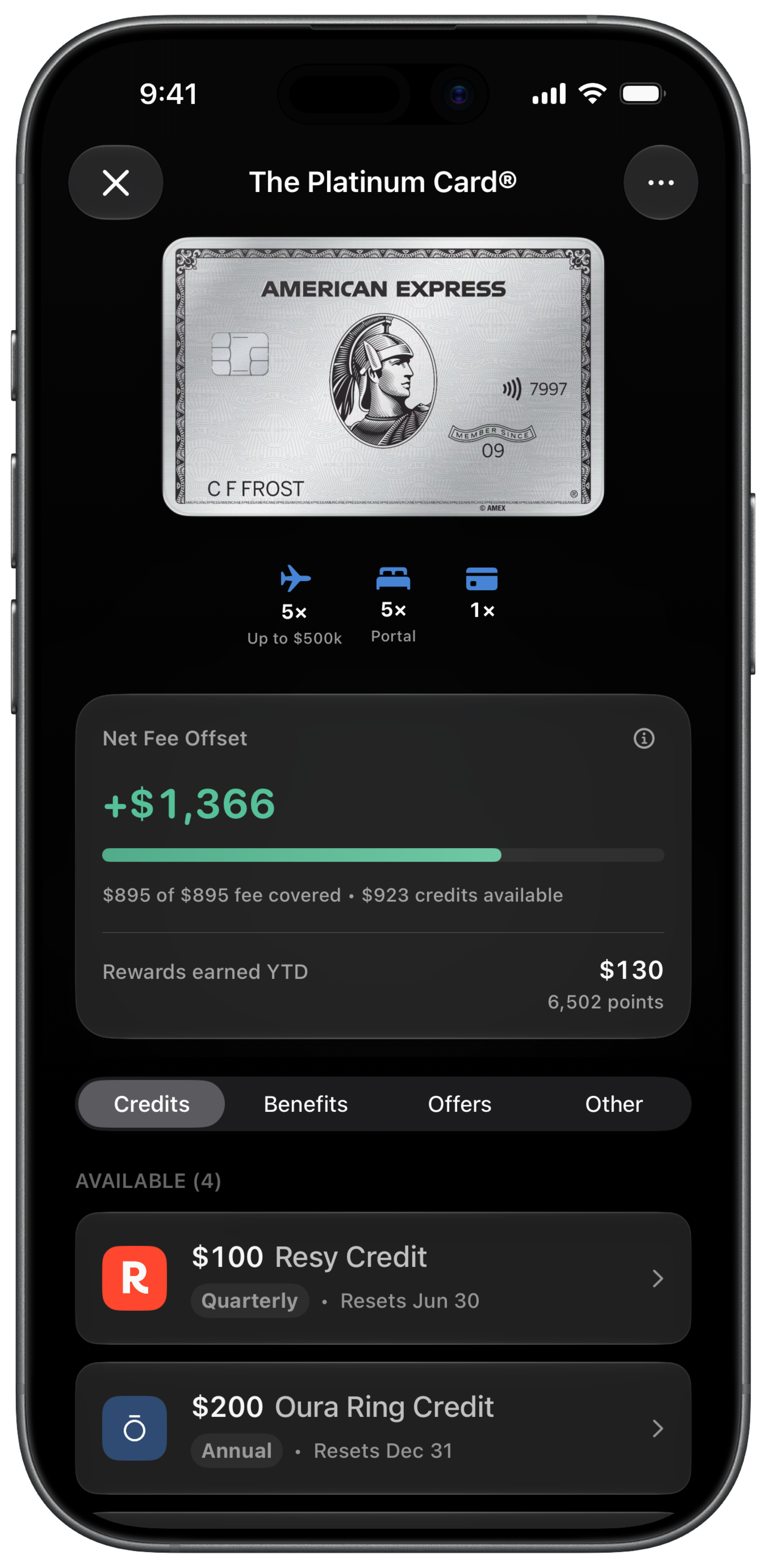

Cards: Amex Platinum + Amex Gold + Blue Business Plus

Total annual fees: $1,220 ($895 + $325 + $0)

For the deep dive on this setup, see the dedicated Amex Trifecta guide.

Which Card for Which Category

| Category | Card | Earn Rate |

|---|---|---|

| Flights | Amex Platinum | 5x MR |

| Hotels (Amex Travel) | Amex Platinum | 5x MR |

| Dining | Amex Gold | 4x MR |

| U.S. Supermarkets | Amex Gold | 4x MR |

| Everything else | Blue Business Plus | 2x MR |

Why It Works

Every dollar earns at least 2x Membership Rewards. Dining and groceries, where most people spend the most, earn 4x. Flights earn 5x. All points pool into one Membership Rewards account with 20+ transfer partners.

The Platinum carries $2,984 in current annual statement credits after the Saks credit ended. If you use even half, the effective fee drops well below $400. The Gold’s credits (up to $424/year) largely offset its $325 fee. The Blue Business Plus costs nothing.

Estimated Annual Value

For someone spending $6,000 on flights, $10,000 on dining, $8,000 on groceries, and $20,000 on everything else:

- Points earned: ~118,000 MR (worth ~$2,360 at 2 cpp via transfer partners)

- Credits used: ~$1,500 (realistic)

- Fees paid: $1,220

- Net value: ~$2,640

Pros and Cons

Pros: Highest earn rates on food and flights. Best lounge access. Massive credit stack. One unified points currency.

Cons: Highest total fee. Amex is not accepted everywhere (especially internationally). Requires a business card for the catch-all slot. Managing the Platinum’s many credits takes effort.

Setup 2: The Chase Trifecta

Cards: Chase Sapphire Reserve (or Preferred) + Chase Freedom Unlimited + Chase Freedom Flex

Total annual fees: $795 (Reserve) or $95 (Preferred) + $0 + $0

Which Card for Which Category

| Category | Card | Earn Rate |

|---|---|---|

| Dining | Sapphire Reserve | 3x UR |

| Flights and hotels (direct) | Sapphire Reserve | 4x UR |

| Flights and hotels (Chase Travel) | Sapphire Reserve | 8x UR |

| Rotating quarterly categories | Freedom Flex | 5x UR |

| Drugstores | Freedom Flex | 3x UR |

| Everything else | Freedom Unlimited | 1.5x UR |

Why It Works

The Chase Trifecta is the gold standard for simplicity. Visa acceptance everywhere. No business card needed. Two no-fee cards handle most spending, and the Sapphire Reserve (or Preferred) provides the premium earning and redemption layer.

Chase Ultimate Rewards transfer to Hyatt, United, Southwest, British Airways, Air France/KLM, and others. The Hyatt partnership alone is one of the most valuable transfer options in the loyalty space. Standard rooms at Park Hyatt properties for 25,000 to 30,000 points per night is difficult to beat.

The Reserve’s $300 travel credit is broad (any travel purchase) and easy to use, unlike some of the narrower Amex credits. That alone brings the $795 fee down to $495 before counting DoorDash, The Edit, Apple, and the rest.

Estimated Annual Value

Same spending profile ($6,000 flights, $10,000 dining, $8,000 groceries, $20,000 everything else):

- Points earned: ~88,500 UR (worth ~$1,550 at 1.75 cpp via transfer partners)

- Credits used: $300 (travel credit)

- Fees paid: $795

- Net value: ~$1,055

Pros and Cons

Pros: Accepted everywhere. Strong transfer partners, especially Hyatt. No business card required. DashPass included on the Reserve.

Cons: Lower earn rates on dining and groceries vs. Amex Gold. Lounge access is Priority Pass and Sapphire Lounges (no Centurion equivalent). More credits to track on the Reserve than the old CSR, but still simpler than Amex Platinum. Freedom Flex quarterly categories require activation and rotate.

Reserve vs. Preferred

If your travel spend is under $5,000 per year and you do not care about lounge access, the Sapphire Preferred at $95 is the better anchor. You lose the 1.5x point multiplier in the Chase travel portal, Priority Pass, and the $300 credit, but the fee is dramatically lower. Compare them directly at Amex Gold vs. Chase Sapphire Preferred.

Setup 3: The Mixed Setup

Cards: Amex Gold + Chase Sapphire Reserve + Capital One Venture X (or Bilt Palladium)

Total annual fees: $1,515 ($325 + $795 + $395) or $1,615 with Bilt Palladium

Which Card for Which Category

| Category | Card | Earn Rate |

|---|---|---|

| Dining | Amex Gold | 4x MR |

| U.S. Supermarkets | Amex Gold | 4x MR |

| Travel bookings | Chase Sapphire Reserve | 4x UR direct / 8x via Chase Travel |

| Flights | Capital One Venture X | 2x miles + portal benefits |

| Hotels via Capital One Travel | Capital One Venture X | 10x miles |

| Everything else | Capital One Venture X | 2x miles |

Why It Works

This setup cherry-picks the strongest card from three different issuers. The Amex Gold is the best dining and grocery card available. The Sapphire Reserve provides the Chase ecosystem (Hyatt transfers, DashPass, Priority Pass) and a clean travel credit. The Venture X adds a second lounge network (Capital One Lounges), 10,000 anniversary miles worth $100, and a $300 travel credit that makes the card effectively $95 per year.

You split your points across three currencies, which is the trade-off. But each currency has strong transfer partners, and the combined earn rate across every category is high.

Estimated Annual Value

Same spending profile:

- Points earned: ~91,000 across three currencies (weighted average ~1.8 cpp)

- Credits used: ~$900 (Gold credits + CSR $300 travel + Venture X $300 travel + 10K anniversary miles)

- Fees paid: $1,515

- Net value: ~$1,015

Pros and Cons

Pros: Best dining earn rate (Gold 4x). Two separate lounge networks (Centurion access via supplemental Platinum not included here, but Capital One Lounges + Priority Pass via CSR). Triple coverage across Visa, Mastercard, and Amex for international acceptance. Strong combined credits.

Cons: Three separate points currencies to manage. More complexity at checkout (“which card for this purchase?”). Higher cognitive overhead than a single-issuer trifecta. No unified pool for large redemptions.

Variant: Swap Venture X for Bilt Palladium

If you pay rent, replacing the Venture X with the Bilt Palladium gives you up to 1.25x on rent and mortgage through Bilt’s housing thresholds, a category no other mainstream transferable-points card matches without a fee workaround. Bilt transfers to Hyatt, American Airlines, United, and others. The fee is $495, so total goes to $1,615, but earning up to 1.25x on a $2,000 to $4,000 monthly housing payment can generate up to 30,000 to 60,000 points per year. That math is still hard to ignore.

How to Choose Your Setup

| Factor | Amex Trifecta | Chase Trifecta | Mixed Setup |

|---|---|---|---|

| Best for | Travelers who eat out | Simplicity-first people | People who want the best of each |

| Total fees | $1,220 | $95–$795 | $1,515–$1,615 |

| Minimum earn rate | 2x | 1.5x | 2x |

| Lounge access | Centurion + Priority Pass | Priority Pass + Sapphire Lounges | Capital One Lounges + Priority Pass |

| Acceptance | Amex not accepted everywhere | Visa accepted everywhere | All three networks |

| Credit complexity | High (12+ credits) | Medium (Reserve has many credits) | Medium (8–10 credits) |

| Points currencies | 1 (MR) | 1 (UR) | 2–3 |

If you want the highest possible earn rates and do not mind managing credits: Amex Trifecta.

If you want something that just works with minimal effort: Chase Trifecta.

If you want to cherry-pick the best card from each issuer and can handle the complexity: Mixed Setup.

The “Which Card Do I Use?” Problem

The biggest practical challenge with any multi-card setup is remembering which card to pull at checkout. It sounds trivial, but it is the reason most people default to one card and leave points on the table.

CardStack solves this directly. It knows your wallet, the merchant you are at, and which card gives the highest estimated value for that purchase. Three cards is very manageable when your phone tells you which one to use.

If you are running a trifecta of any kind, a tool that answers “which card here?” is the difference between theoretical value and actual value.

Final Thoughts

There is no single best three-card setup. There is the best one for how you spend, how much complexity you are willing to manage, and whether you value transfer partner flexibility or simplicity.

Start with one of these three frameworks, adjust based on your actual spending patterns, and pay attention to which credits you are actually using versus which ones expire unused. The best wallet is the one you actually use well, not the one that looks best on a spreadsheet.

Get $500+ a year back from your premium cards.

CardStack tracks every credit, offer, and renewal across your wallet so unused perks do not slip past their reset dates.

CardStack Insiders

Newsletter

Card news, standout deals, and product updates—straight to your inbox.

By signing up, you agree to ourTermsandPrivacy Policy. Unsubscribe anytime.

Read Next

Related articles