Amex Offers vs Chase Offers: Which Bank's Deals Are Actually Better?

Amex Offers vs Chase Offers in 2026: how each program works, where the value differs, why people miss them, and how to auto-activate both.

Amex Offers and Chase Offers are the same idea wearing different logos: targeted merchant deals inside your card account that pay a statement credit when you spend at a specific merchant. They are also the most consistently wasted value in credit cards, because both programs require you to manually activate each offer before you pay — and almost nobody does that reliably.

I’ve written before about how Amex Offers work. This piece puts the two programs side by side, because if you carry both an Amex and a Chase card — and most points people do — you are managing two separate offer systems with different rules, different interfaces, and the same failure mode.

TL;DR

- Same core mechanic: add the offer to a specific card first, pay with that card, credit posts after the charge

- Amex Offers tend to run richer and broader — travel, retail, dining, subscriptions — and premium cards often see premium-merchant targeting

- Chase Offers skew toward everyday spend (groceries, gas, retail, services) and are often percentage-based with a cap

- Both are personalized and per-card — your Platinum, Gold, Sapphire, and Freedom each have their own list

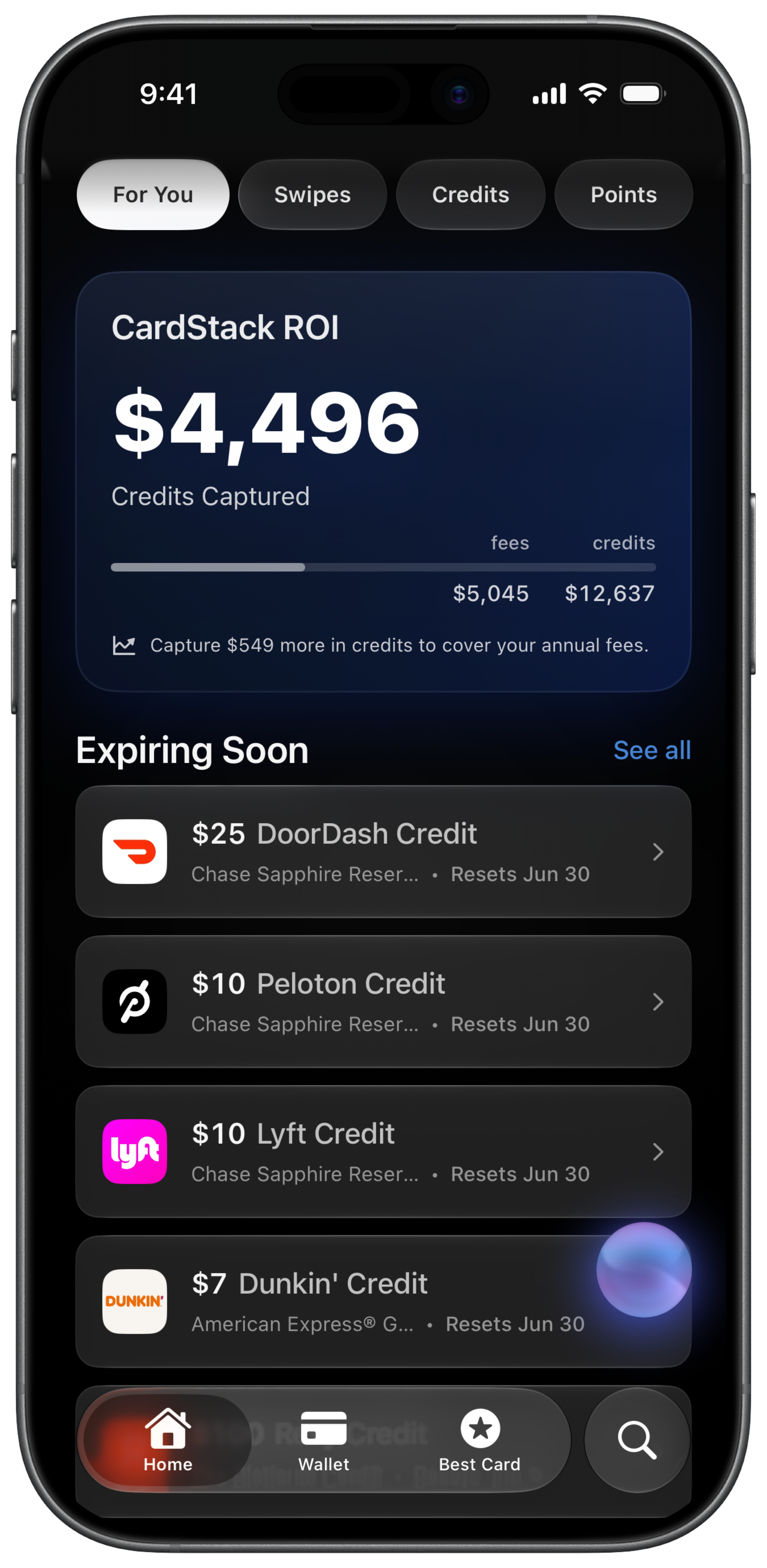

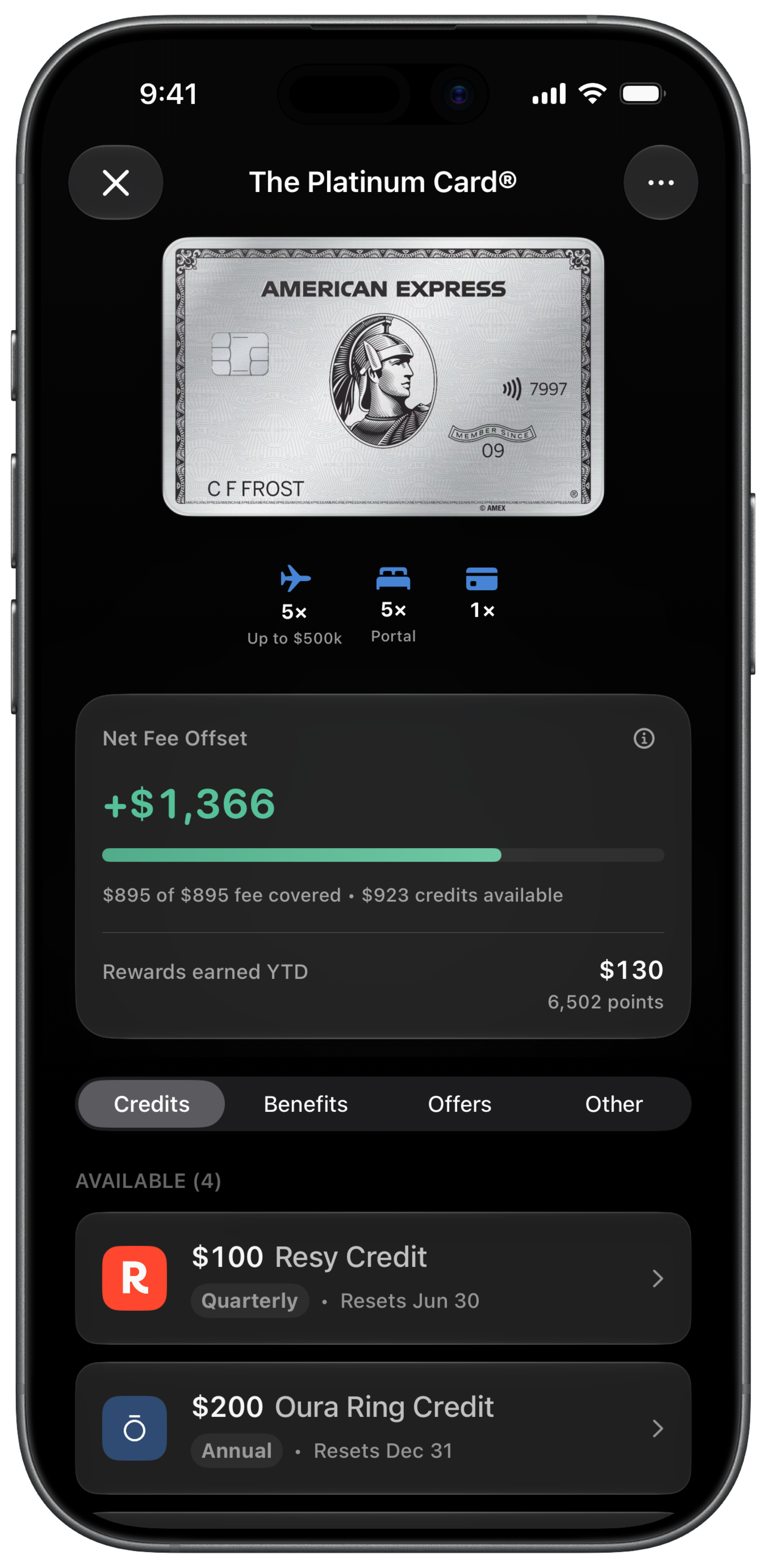

- The real comparison isn’t Amex vs Chase — it’s activated vs forgotten. The CardStack browser extension auto-activates both

How each program works

| Amex Offers | Chase Offers | |

|---|---|---|

| Where they live | Amex app / americanexpress.com, per card | Chase app / chase.com, per card |

| Activation | ”Add to Card” before purchase | ”Add offer” before purchase |

| Typical structure | ”Spend $X, get $Y back” or bonus points | Often ”% back, up to $Y cap” |

| Payout | Statement credit (or Membership Rewards, on points offers) | Statement credit |

| Targeting | Personalized per cardholder and card | Personalized per cardholder and card |

| Expiration | Fixed deadline per offer; popular ones can hit enrollment caps early | Fixed deadline per offer, frequently shorter windows |

| Reusability | Mostly one-time use | Mostly one-time use |

The structural rules that matter are identical:

- Activation must come before the purchase. A qualifying charge with no prior activation earns nothing, and there is usually no retroactive fix.

- Offers are card-specific. Adding an offer on your Amex Platinum does nothing for your Amex Gold. Same on the Chase side across a Sapphire Reserve and a Freedom.

- Offers are targeted. Two people with identical cards see different lists. If your friend has a great offer and you don’t, that’s the program working as designed.

Where Amex Offers win

Deal size and merchant quality. Amex’s list regularly includes hotels, airlines, and larger retail brands, and the headline deals run bigger — offers in the “spend $250+, get $50 back” range show up with some regularity, especially on premium cards. A single good travel offer can be worth more than a year of small grocery deals.

Points offers. Some Amex Offers pay bonus Membership Rewards instead of statement credits. At the ~2.0 cents-per-point valuation in our points value chart, a 5,000-point offer is ~$100 of transfer-partner value — often better than the equivalent cash offer.

Volume. Amex cardholders routinely have dozens of offers sitting on each card. That’s good (more chances to match your spending) and bad (nobody scrolls the whole list weekly, which is how offers get missed).

Where Chase Offers win

Everyday relevance. Chase’s mix skews toward merchants normal spending actually hits — grocery chains, gas stations, pharmacies, streaming, local services. You’ll trigger these without planning a trip.

Percentage structure. A “10% back up to $12” offer at a grocery store you already shop at takes no extra work. The caps keep individual offers small, but the hit rate is higher.

Simplicity of stacking with the household cards. Chase Offers appear across the Freedom and Sapphire lines alike, so the no-annual-fee cards in a Chase trifecta get their own lists too.

The honest verdict

If you forced me to pick one program, Amex Offers has the higher ceiling — the deals are bigger and the points offers are undervalued by most people. Chase Offers has the higher floor — you’ll capture more of them without changing behavior.

But picking is the wrong frame. The expected value of either program is dominated by one variable: activation rate. A mediocre offer you activated is worth infinitely more than a great one you didn’t. Both banks designed programs where the default outcome is forgetting, and both profit from that default.

The rules that eat people’s credits

A few failure modes account for nearly every “my offer didn’t pay” complaint, on both sides:

- Wrong card. You added the offer on card A and paid with card B. The lists are per-card; so is the payout.

- Expired before you shopped. Chase windows in particular can be short. Check the date when you activate.

- Terms exclusions. Online-only, in-store-only, excluded subsidiaries, minimum spend not met, or third-party payment processors (a restaurant that rings through a delivery app, a purchase through PayPal) breaking merchant matching.

- Gift card purchases. Frequently excluded by terms even when the charge goes through.

- The one-time offer already fired. Most offers are single-use; the second purchase earns nothing.

The test I use before counting any offer as money: would I make this exact purchase without the offer? If yes, activate and enjoy. If no, it’s not a reward — it’s a coupon trying to change your behavior, and the bank wins that trade more often than you do.

Auto-activating both (the part that actually fixes this)

Activating offers is a chore with no intellectual content: open the app, scroll, tap Add, repeat, across every card, forever. This is precisely the kind of work software should do.

The CardStack browser extension — available for Chrome and Safari — automates it for both issuers. When you’re logged into americanexpress.com or chase.com, it detects the available offers on your cards and adds them automatically. Every offer, every card, no scrolling. From then on, any qualifying purchase just triggers its credit.

That flips the default. Instead of capturing the three offers you happened to notice, you capture every offer that happens to overlap your real spending — which is the only version of these programs that is worth counting at face value. The CardStack iOS app then tracks the credits as they post, alongside your statement credits and annual fees, so you can see what the offers actually paid you over the year.

Bottom line

Amex Offers bring bigger deals and points upside; Chase Offers bring everyday hit rate. Carry both issuers and you should be working both lists — or better, letting the CardStack extension work them for you while you spend exactly the way you were going to anyway.

The banks built the friction on purpose. Automating it away is the whole game.

Get $500+ a year back from your premium cards.

CardStack tracks every credit, offer, and renewal across your wallet so unused perks do not slip past their reset dates.

CardStack Insiders

Newsletter

Card news, standout deals, and product updates—straight to your inbox.

By signing up, you agree to ourTermsandPrivacy Policy. Unsubscribe anytime.

Read Next

Related articles