The 3-Card Setup That Covers 90% of Spending

The Amex Trifecta (Platinum, Gold, and Blue Business Plus) routes every major spending category to its highest earn rate. Here's how the setup works.

You do not need eight credit cards to have a strong wallet. Most people do not need five. If you want a setup that covers nearly every spending category at a strong earn rate, pools all your points into a single program, and is actually manageable day to day, three cards will do it.

The Amex Trifecta has been my foundation for years. Three cards. One points currency. No major category earning 1x if you can help it.

Here is exactly how it works and why it is the strongest three-card setup available for anyone building toward travel.

TL;DR

- Amex Platinum: 5x on flights, lounge access, $1,500+ in annual credits, use for every flight booking ($895 fee)

- Amex Gold: 4x on dining and 4x on U.S. groceries, use for every restaurant and grocery run ($325 fee)

- Blue Business Plus: 2x on everything else, the no-fee catch-all that fills every gap ($0 fee)

- Total: $1,220 in annual fees, no category earning less than 2x

- Optional 4th card: Bilt Palladium if you pay rent

Why Three Cards Instead of One

The appeal of a single card is real. One bill, one login, no card-selection decisions at checkout. Cards like the Chase Sapphire Reserve or Capital One Venture X try to do most things adequately at 3x or 2x across broad categories.

The problem is adequately.

If you spend $1,500 a month on dining and groceries and use a 2x card, you earn 3,000 points. The same spend on the Amex Gold earns 6,000 points. Over a year, that gap is 36,000 Membership Rewards points, worth roughly $720 in business class flights at a conservative transfer rate. That is money left on the table every single year, from one category.

The Amex Trifecta does not ask you to give anything up. Every card serves a specific role. The overhead is minimal, three decisions at checkout instead of one.

The Three Cards and Their Jobs

The Amex Platinum, Flights and Lounge Access

The Platinum has one primary job in this setup: book every flight on it.

5x Membership Rewards on flights booked directly with airlines or through Amex Travel is one of the highest-value airfare earn setups on a personal card when paired with strong redemptions. If you spend $8,000 per year on flights (not unusual for someone who travels three or four times a year) that is 40,000 points. At 2 cents per point through transfer partners, that is $800 in travel value from flights alone.

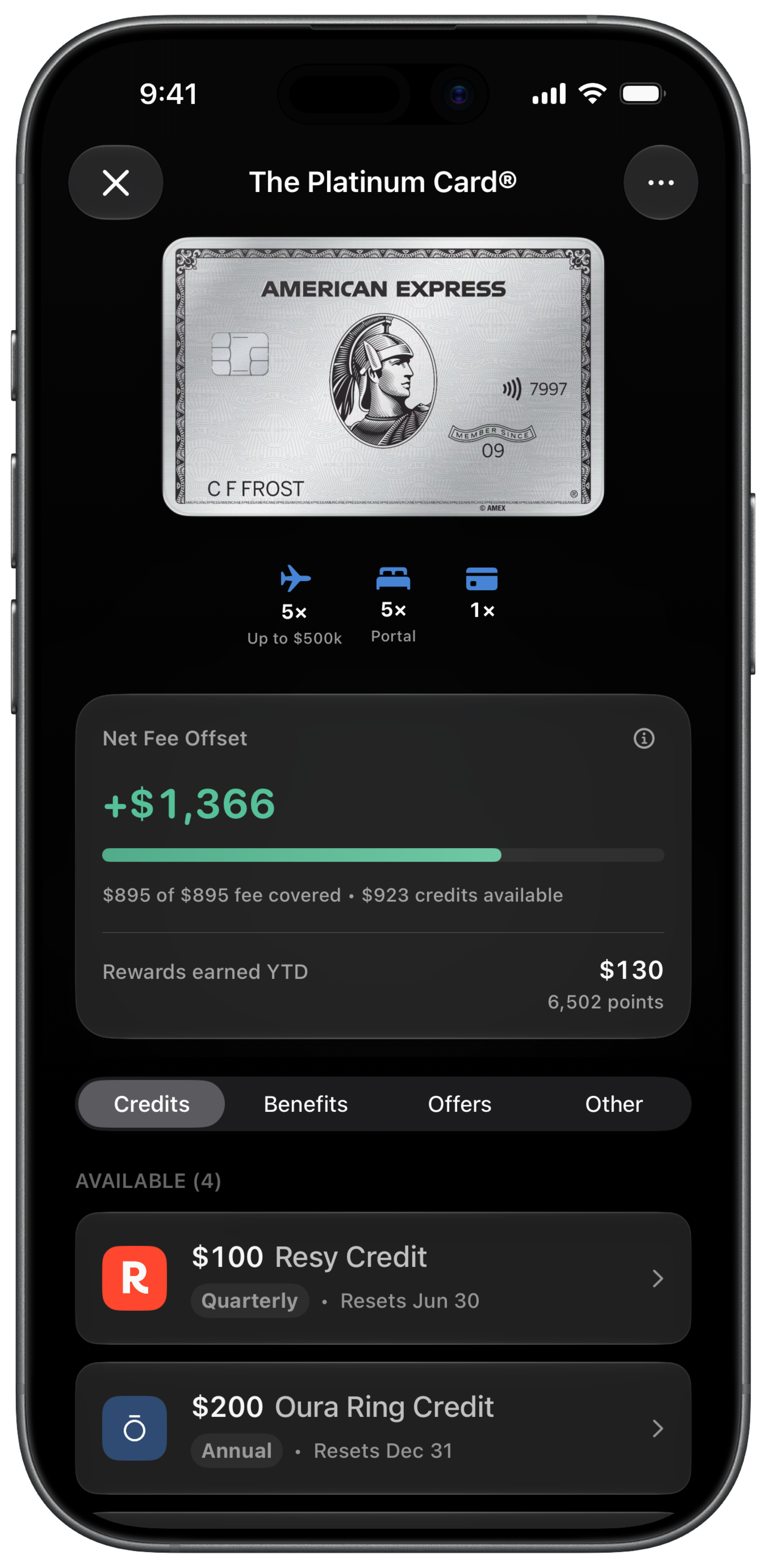

The Platinum also brings everything that makes travel better: Centurion Lounge access, Priority Pass, Hilton and Marriott Gold status, and a long list of credits that, when used, offset most of the $895 annual fee. The hotel credit ($600), Resy credit ($400), entertainment credit ($300), Uber Cash ($200), Walmart+ credit ($155), airline fee credit ($200), Lululemon ($300), and CLEAR ($209) alone total $2,164 in potential annual value before Equinox, Oura, and Uber One. The former Saks credit ended June 30, 2026 and is no longer redeemable.

You will not use all of them. Most people extract $1,200 to $1,600 in credits, which brings the effective cost of the card well below its face-value fee.

In the trifecta, the Platinum is the premium layer. You use it on flights and for its credits and perks. Nothing else.

The Amex Gold, The Workhorse

The Gold is where most of your day-to-day points are made.

4x at restaurants worldwide. 4x at U.S. supermarkets (up to $25,000 per year). If you eat at restaurants and buy groceries (which everyone does) this card earns more points on those purchases than any other transferable points card available.

The math is simple. Say you spend $800 a month dining out and $700 a month on groceries. That is $1,500 a month in food spend, all at 4x. You are earning 6,000 points per month (72,000 per year) just on food. At $720 in transfer partner value, the $325 annual fee is covered in the first five months.

The Gold also earns 3x on flights booked directly, though in the trifecta you will typically use the Platinum for flights to get 5x instead of 3x.

The credits on the Gold ($120 Uber Cash, $120 dining credit at select partners, $100 Resy semi-annual, plus $84 Dunkin’ and $100 Hotel Collection) are a bonus. They make the fee even easier to justify. But the reason you carry this card is the 4x on food.

The Blue Business Plus, The Silent Foundation

The Blue Business Plus is the least glamorous card in the setup and possibly the most important one.

It earns 2x Membership Rewards on all purchases up to $50,000 per year. No annual fee. No categories. No exceptions.

Every dollar that does not fall into the Platinum’s flight category or the Gold’s dining and grocery category goes here. Online shopping. Subscriptions. Gas. Utilities. Gifts. Random purchases that do not fit a bonus category anywhere else.

Without the Blue Business Plus, those purchases earn 1x on the Platinum or Gold. With it, they earn 2x. That is a 100% increase in earn rate on every gap in the setup, for free.

Technically a business card, the BBP is widely used by people with any form of self-employment or freelance income. If that applies to you, every legitimate business expense (software, equipment, contractor payments, advertising) earns 2x and feeds directly into the same Membership Rewards pool.

The points go into the same bucket as your Platinum and Gold points. One pool. One strategy. One transfer when it is time to book a flight.

The Combined Earn Rate

Here is what the full trifecta covers:

| Category | Card | Earn Rate |

|---|---|---|

| Flights (direct / Amex Travel) | Amex Platinum | 5x |

| Dining worldwide | Amex Gold | 4x |

| U.S. supermarkets | Amex Gold | 4x |

| Everything else | Blue Business Plus | 2x |

Nothing in your daily life earns less than 2x. Dining and groceries earn 4x. Flights earn 5x.

Compare that to what most single-card setups offer: 2x to 3x on a few bonus categories, 1x on everything else. The trifecta eliminates that 1x baseline almost entirely.

The Math on $1,220 in Annual Fees

The total cost of the trifecta is $895 + $325 + $0 = $1,220 per year.

That sounds significant until you account for credits.

The Platinum alone offers $600 in hotel credits, $400 in Resy dining, $200 in Uber Cash, $300 in entertainment, and $155 in Walmart+. If you use even half of that conservatively, you are getting $800+ back in credits, bringing your effective Platinum cost to under $100.

The Gold adds $120 Uber Cash, $120 in dining credits, and $100 in Resy semi-annual, up to $424 in total credits if you use everything. That is $99 more than the $325 fee. The Gold effectively costs nothing if you use the credits you care about.

Realistic combined credits used: $1,200 to $1,600. Realistic combined annual fees: $1,220. Before you earn a single point, the trifecta is at break-even or better for anyone who travels, eats out, and uses a handful of the credits.

The points are pure upside.

Why Membership Rewards Is the Right Currency

All three cards feed the same Amex Membership Rewards pool. That is the structural advantage of the trifecta over mixing programs.

When you accumulate points across Membership Rewards, you have 20 transfer partners available, Air Canada Aeroplan, ANA, Singapore Airlines, Air France/KLM Flying Blue, British Airways, Delta SkyMiles, Marriott Bonvoy, Hilton Honors, and more. The breadth of partners means you can chase sweet spots across multiple programs rather than being locked into one airline or hotel chain.

The best redemptions (business class flights, premium hotels) typically come from transfers rather than direct Amex Travel bookings. If you are redeeming for cash or statement credits, you are leaving most of the value on the table. Use the points-vs-cash calculator to see exactly what your balance is worth before you redeem.

The Optional 4th Card: Bilt for Rent

The Amex Trifecta covers flights, dining, groceries, and everything else. There is one major category it cannot touch: rent.

No Amex card earns points on rent payments. For most people, rent is the largest fixed monthly expense they have. Paying $3,000 to $5,000 a month in rent and earning zero points on it is one of the most significant missed opportunities in personal finance.

The Bilt Palladium fixes this. It earns up to 1.25x Bilt Rewards on rent and mortgage payments through Bilt’s housing thresholds with no transaction fee. It also earns 2x on everything else, overlapping with the Blue Business Plus as a catch-all for personal purchases you may not want on a business card.

Bilt Rewards transfer to World of Hyatt, American Airlines, United, and a growing list of partners. Hyatt redemptions in particular (Park Hyatt properties, Andaz resorts, Alila hotels) deliver some of the best hotel value available anywhere in the loyalty space.

If you pay rent and want to earn on it, the Bilt Palladium is the natural complement to the Amex Trifecta. The total fee stack goes from $1,220 to $1,715, but the earn rate on your largest monthly expense goes from 0x to up to 1.25x, a meaningful gain if your rent is substantial.

If the $495 Palladium fee is too high, the standard Bilt Blue Card has no annual fee and still earns on rent. You give up some perks, but the fundamental benefit (earning on rent) stays intact.

Who This Setup Is For

The Amex Trifecta is the right starting point if you:

- Travel at least a few times a year and want lounge access and strong flight earn rates

- Spend meaningfully on dining and groceries every month

- Want all your points in one program rather than split across multiple currencies

- Are comfortable with a combined fee of $1,220 and can realistically use enough credits to offset it

- Plan to redeem through transfer partners for flights or hotels rather than cash back

- Have any self-employment income or business expenses that qualify for the Blue Business Plus

Who Should Skip It

This setup is not ideal if you:

- Prefer cash back over points, the Amex ecosystem is built for travel redemptions

- Cannot qualify for the Platinum or Gold due to credit history or income constraints

- Spend very little on dining and groceries and the Gold’s earn rate would not justify $325

- Travel rarely and the Platinum’s fee is hard to offset through credits

- Are locked out of Amex cards due to the Amex application rules (generally one card per 90 days, no more than two cards per 90 days)

If you are earlier in your credit journey, a Chase Sapphire Preferred plus a no-fee catch-all is a better starting point. Build toward the trifecta once you have the credit profile and spending volume to support it.

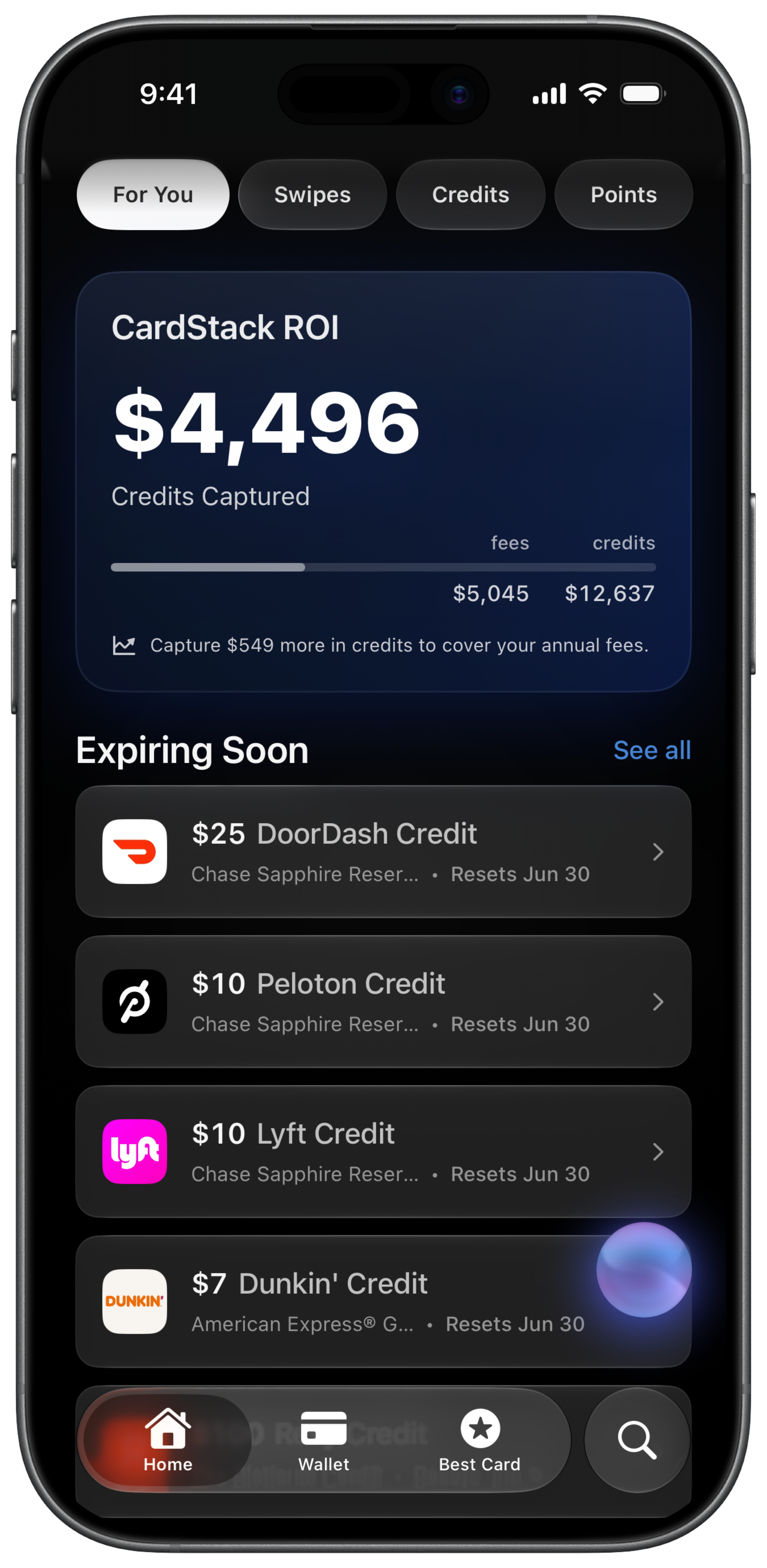

Keeping Track of It All

Three cards means three sets of credits, three reset schedules, and three statements to review. The Platinum alone has credits resetting monthly, quarterly, and semi-annually across a dozen categories.

This is not a theoretical problem. Miss the second-half Resy credit on the Platinum and you are down $200. Forget to use the Gold’s dining credit three months in a row and you have left $30 on the table. Small amounts individually, significant when compounded across a full year.

CardStack tracks all of it automatically. Which credits you have used, what is expiring, and how your annual fee is performing across every card in your wallet. A three-card setup is very manageable with the right tool. Without one, the credits that make the math work are the first thing to fall through the cracks.

Final Verdict

The Amex Trifecta is the most efficient three-card setup for anyone who travels and wants to stop earning 1x on the majority of their spending.

Platinum on flights. Gold on food. Blue Business Plus on everything else. Every major category covered at 2x minimum, with 4x and 5x where it matters most. All points in a single Membership Rewards pool that transfers to 20 partners.

The combined fee of $1,220 is real, but the Platinum credits alone offset most of it for anyone who travels and uses a handful of the benefits. The Gold’s credits cover its own fee. The Blue Business Plus costs nothing.

You do not need eight cards. You need three, and a system for actually using what you are paying for.

Get $500+ a year back from your premium cards.

CardStack tracks every credit, offer, and renewal across your wallet so unused perks do not slip past their reset dates.

CardStack Insiders

Newsletter

Card news, standout deals, and product updates—straight to your inbox.

By signing up, you agree to ourTermsandPrivacy Policy. Unsubscribe anytime.

Read Next

Related articles