My 2026 Credit Card Wallet Setup

Eight cards, $2,855 in annual fees, and a clear reason for every single one. Here's exactly how I use them and why.

I carry eight credit cards. I know how that sounds.

Most personal finance advice tells you to simplify, pick one or two cards, keep it clean, do not overthink it. That advice is reasonable for most people. But if you spend heavily across a few specific categories, travel internationally a few times a year, and are willing to put in the work to actually use the cards you carry, a multi-card setup can generate a significant amount of value.

My total annual fees are $2,855. What I get back (in credits, points, hotel perks, and lounge access) is meaningfully more than that. Not because I am doing anything complicated. Because each card has one job, and I am deliberate about using the right card at the right time.

Here is the full setup.

TL;DR

- Amex Platinum, lounges, 5x flights, travel benefits ($895)

- Amex Gold, 4x dining and groceries ($325)

- Bilt Palladium, rent & mortgage through Bilt plus 2x on everything else ($495)

- Capital One Venture X, Turkish Airlines business class, 2x catch-all ($395)

- Marriott Bonvoy Brilliant, Marriott status and the Maldives ($650)

- Chase Sapphire Preferred, World of Hyatt transfers ($95)

- Blue Business Plus, 2x on all business expenses ($0)

- Prime Visa, Amazon and Whole Foods ($0)

Total annual fees: $2,855. Total no-fee cards pulling weight: 2.

Why Eight Cards

Every card in this wallet has a specific reason it exists. Nothing is here because of a sign-up bonus I never canceled. Nothing is here out of habit.

The way I think about it: every dollar you spend is a routing decision. If you spend $3,000 a month on groceries, dining, rent, Amazon, flights, and business expenses (and you put all of that on one card) you are leaving earn rate on the table every single month. The multi-card setup is just routing each dollar to the highest return.

The cost is complexity. You have to remember which card to use where. You have to track credits across monthly, quarterly, and semi-annual reset schedules. You have to stay on top of expiration windows.

I will come back to how I handle that.

The Wallet, Card by Card

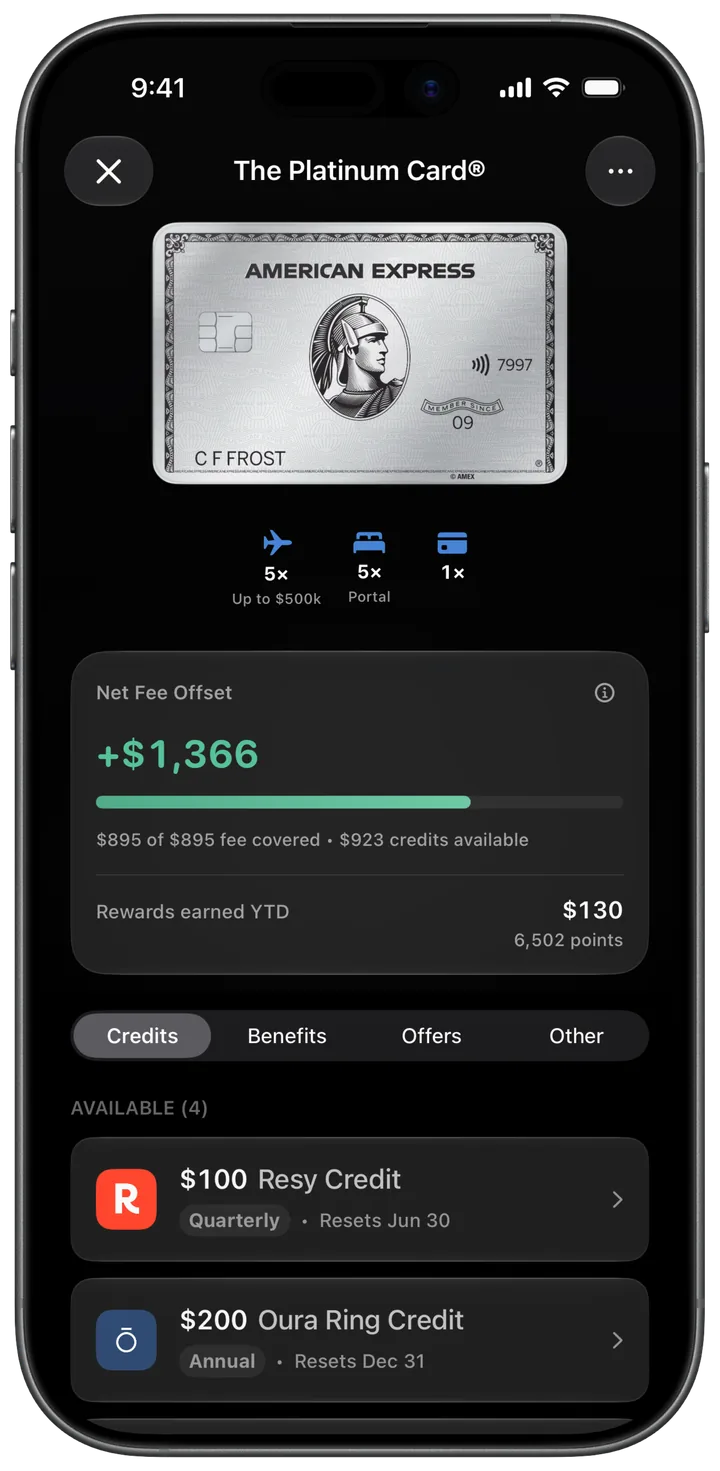

The Amex Platinum, Benefits and Lounge Access

The Platinum is the most expensive card I carry and the hardest to defend to people who have never used it. At $895, you are paying nearly $75 a month. What makes it work is Centurion Lounge access, 5x on direct flight bookings, and a long list of credits that (if you use them) more than offset the fee.

My math on the Platinum: $600 in hotel credits, $400 Resy dining, $300 entertainment, $200 Uber Cash, $155 Walmart+, $200 airline fee credit, and $209 CLEAR Plus. I use most of those. The Lululemon and Oura Ring credits I do not, so I back those out.

The fee effectively nets to zero or better. And then I get Centurion Lounge access on top of it.

I also use it as my primary flight card. 5x on direct bookings goes straight into Membership Rewards, which I use primarily for business class on Aeroplan and ANA. The Platinum is the engine of the whole setup.

The Amex Gold, Food Is Where Points Are Made

The Gold exists for one reason: 4x on dining at restaurants worldwide and 4x at U.S. supermarkets.

If I am at a restaurant or buying groceries, the Gold comes out. Every time. No exceptions.

The credits help ($120 Uber Cash, $120 dining credit, $100 Resy) but the real reason I have this card is the earn rate. Between restaurants and groceries, my household spends roughly $2,500 a month in those categories. That is 10,000 Membership Rewards points per month (120,000 points per year) on food alone. At 2 cents per point, that is $2,400 in travel value from spending I was doing regardless.

The Gold pays for itself in earn rate within the first month.

Bilt Palladium, Getting Paid to Pay Rent

The Bilt Palladium is the most underrated card in my wallet for one reason: rent.

Most credit cards do not earn points on rent. Bilt does. My rent is one of my largest fixed monthly expenses, and every dollar of it can now earn up to 1.25x Bilt Rewards points instead of nothing. On a $4,000 rent payment, that is up to 5,000 points per month (60,000 per year) on a category that most people earn zero on.

The Palladium tier also earns 2x on everything else, which makes it a strong catch-all for purchases that do not fall into a bonus category on my other cards. It transfers to Hyatt, American Airlines, United, and a handful of airline and hotel partners, so the points are flexible.

At $495 per year, the Palladium is one of the harder fees to justify if you do not pay a lot in rent. But if housing is a significant line item in your monthly spending, getting any meaningful earn on that purchase is still a huge upgrade over 0x.

Capital One Venture X, Turkish Airlines and a Clean Catch-All

The Venture X exists in my wallet for one very specific reason: Turkish Airlines Miles & Smiles.

Capital One transfers to Turkish at a 2:1.5 ratio, and Turkish’s award chart is one of the most underrated in the business. Business class on United to Europe through Turkish is significantly cheaper in miles than booking directly. I have used this redemption twice. It is the kind of sweet spot that makes you feel like you are gaming the system legally.

Beyond that, the Venture X earns 2x on everything, which makes it useful as a backup catch-all. The $300 travel credit covers the $395 fee. The Priority Pass access adds lounge coverage for airports where I do not have Centurion access. It is a well-rounded card that more than justifies itself on the Turkish Airlines angle alone.

Marriott Bonvoy Brilliant, The Maldives Card

I will be honest about this one. The Marriott Bonvoy Brilliant is in my wallet because I love Marriott hotels, and specifically because the Maldives is my favorite place on earth.

St. Regis Maldives. W Maldives. The Ritz-Carlton Maldives. These are Marriott properties, and points redemptions there (especially during off-peak windows) can represent extraordinary value. A suite that costs $2,000 per night booking direct might redeem for 60,000 to 80,000 Marriott Bonvoy points. The Brilliant earns 6x at Marriott properties and comes with automatic Marriott Platinum Elite status, which brings suite upgrades and lounge access at most properties.

The $650 annual fee is steep. The $300 dining credit helps offset it. The Marriott status is the reason I keep it, I would lose Platinum Elite without it, and Platinum Elite at a St. Regis Maldives is a different experience than standard.

If Marriott is not your hotel chain, this card is hard to justify. For me, it is the card that makes the best trips significantly better.

Chase Sapphire Preferred, The Hyatt Key

The Chase Sapphire Preferred is the cheapest card in my wallet at $95 and possibly the most strategically important.

I hold it because I need access to Chase Ultimate Rewards transfer partners, specifically World of Hyatt. Hyatt is the best hotel loyalty program available for premium redemptions. Park Hyatt properties that cost $800 per night often redeem for 25,000 to 35,000 points. The math does not get better than that in hotel loyalty.

The Sapphire Preferred earns 3x on dining and 3x on online grocery purchases, which I use as a backup when I am out of Gold and want the Chase points instead of Membership Rewards. The $95 fee is justified by a single Hyatt redemption per year.

I could upgrade to the Reserve for better earn rates, but I already have the Platinum and Venture X covering lounge access. The Preferred keeps my Chase point pipeline open without doubling up on benefits I already have.

Blue Business Plus, Every Business Expense, 2x

The Blue Business Plus has no annual fee and earns 2x Membership Rewards on all purchases up to $50,000 per year.

Everything business-related goes on this card. Software subscriptions, domain registrations, contractors, equipment. Categories that do not hit bonus rates on my personal cards route here automatically. The points flow into the same Membership Rewards pool as my Platinum and Gold, which makes them flexible and valuable.

A no-fee card earning 2x on business spend is not glamorous. It is just correct. I would feel silly putting business expenses on a 1x card when this exists.

Prime Visa, Amazon and Whole Foods, Done

The Prime Visa earns 5% back at Amazon and Whole Foods, which for me means cash back on a significant volume of purchases. Amazon is where I buy most of what I need that is not groceries or food. Whole Foods is my grocery store of choice in cities where it is available.

The card has no annual fee and requires a Prime membership, which I have. It does not earn transferable points. It earns cash back. For the Amazon and Whole Foods category specifically, 5% cash back often beats what I could earn in Membership Rewards points, even after accounting for transfer partner upside.

This is the pure utility card in the setup. No strategy. Just 5% on two of my most consistent spending categories.

What This Setup Is Built For

When I look at the full wallet, it routes every major spending category to the best possible earn rate:

| Category | Card | Earn Rate |

|---|---|---|

| Rent & Mortgage | Bilt Palladium | Up to 1.25x Bilt Rewards |

| Flights (direct) | Amex Platinum | 5x Membership Rewards |

| Dining | Amex Gold | 4x Membership Rewards |

| Groceries (US) | Amex Gold | 4x Membership Rewards |

| Amazon / Whole Foods | Prime Visa | 5% cash back |

| Marriott hotels | Bonvoy Brilliant | 6x Bonvoy points |

| Business expenses | Blue Business Plus | 2x Membership Rewards |

| Everything else | Bilt Palladium or Venture X | 2x |

The gaps (parking, utilities, random one-off spending) go to Bilt or Venture X at 2x. There is no major category earning 1x.

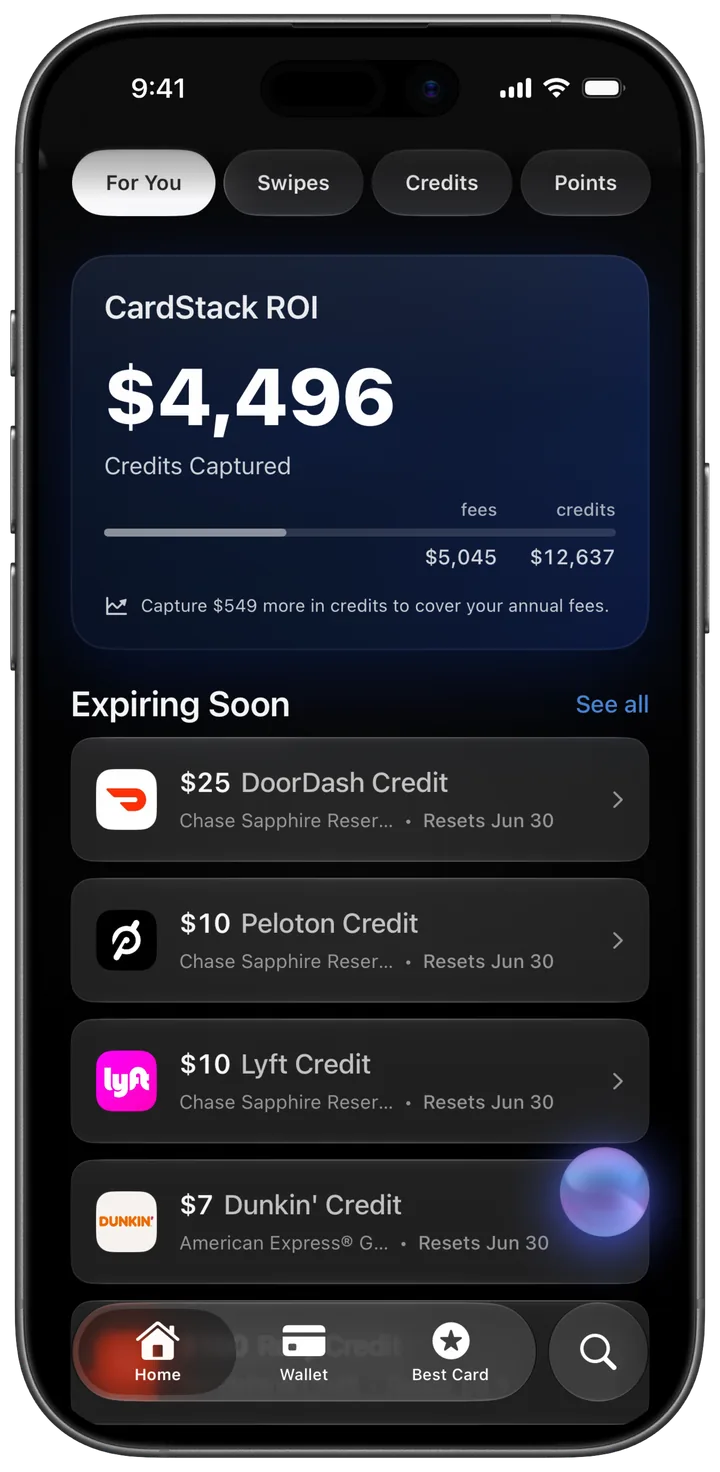

The Part Nobody Talks About

Here is the problem with an 8-card wallet: the credits.

Between the Platinum, Gold, Venture X, Brilliant, and Sapphire Preferred, I have credits resetting monthly, quarterly, semi-annually, and annually. Some require specific portals. Some have narrow partner lists. Some expire at the end of December and you get exactly one chance to use them.

I have missed credits before. A $50 Saks credit I forgot to use in the second half of the year — back when the benefit still had a Jul–Dec window before ending June 30, 2026. A quarterly Resy credit I let lapse. It is not a lot of money individually, but across 8 cards, the missed credits add up quickly.

This is exactly why I built CardStack. It is the app that tracks which credits I have used, what is still available, what is expiring soon, and what my annual fee performance looks like across every card. I used to manage this in a spreadsheet. Then in my head. Neither worked reliably. The app is the only thing that made an 8-card wallet actually manageable.

If you are running a multi-card setup and you are not tracking it properly, you are probably paying for benefits you are not using. That is money you are handing back to the bank every time a credit expires unclaimed.

Who Should and Should Not Try This

This setup makes sense if you:

- Pay meaningful rent every month and want to earn on it

- Spend heavily on dining and groceries and want 4x on both

- Fly internationally and care about specific transfer partner sweet spots (Hyatt, Turkish, Aeroplan)

- Are loyal to a specific hotel chain and want status to actually matter

- Have business expenses that deserve a dedicated card

- Are willing to actively track and use credits across multiple reset schedules

This setup does not make sense if you:

- Prefer to minimize mental overhead around credit cards

- Do not spend enough in any single category to justify a specialized card for it

- Are not planning to redeem points through transfer partners, the math only works at 1.5 to 2 cents per point, not at cash redemption rates

- Are early in building your credit and cannot qualify for premium cards yet

- Cannot float multiple annual fees before the credits offset them

Final Verdict

Eight cards sounds excessive until you see what each one is doing.

The Platinum handles flights and lounge access. The Gold handles food. The Bilt handles rent. The Venture X handles Turkish Airlines and everything else. The Brilliant handles Marriott. The Sapphire Preferred handles Hyatt. The Blue Business Plus handles work. The Prime Visa handles Amazon.

No dollar in my wallet earns 1x if I can help it.

The total fee is real, $2,855 is not trivial. But the credits across those cards, combined with the earn rates, deliver significantly more than that in realized value each year. The key word is “realized.” You have to use the credits. You have to book with the right card. You have to actually redeem your points for something valuable rather than cash back at a third of the value.

If you want to try a setup like this, start with one or two cards that match your biggest spending categories. Add cards only when you have a specific reason, a transfer partner you want access to, a hotel chain you are loyal to, a spending category you are leaving on the table.

And then, once the complexity starts to grow, track it properly. Because a credit that expires is not a benefit. It is a donation to the bank.

Get $1000+ a year back from your premium cards.

CardStack tracks every credit, offer, and renewal across your wallet so unused perks do not slip past their reset dates.

CardStack Insiders

Newsletter

Card news, standout deals, and product updates—straight to your inbox.

By signing up, you agree to ourTermsandPrivacy Policy. Unsubscribe anytime.

Read Next

Related articles