Should You Keep or Cancel Your Credit Card? A Decision Framework

A step-by-step framework to decide if a card's annual fee is worth paying. Includes a checklist you can use for every card, every year.

Every year, your annual fee hits and you have the same internal debate: is this card still worth it? For a $95 card, the stakes are low. For an $895 card, it is a real financial question.

Most people either auto-renew without thinking (and miss credits they could have used) or cancel reflexively at the fee (potentially losing benefits worth more than the fee). Neither is a good strategy.

Here is a structured framework you can use for every card, every year. Six steps, one decision.

TL;DR

- Calculate your effective annual fee (fee minus credits used)

- Value the non-credit benefits you actually use

- Call for a retention offer before deciding

- Check downstream impacts (credit score, points, perks)

- Compare alternatives

- Make the decision: keep, downgrade, or cancel

- When effective fee + retention offer makes the card free or close to it: keep

- When effective fee is high and you are not using key benefits: cancel or downgrade

Step 1: Calculate Your Effective Annual Fee

This is the foundation of the decision. Before anything else, figure out what you are actually paying.

Effective Annual Fee = Listed Fee − Credits You Used in the Past 12 Months

Pull up your last year of statements and count only the credits that actually posted, not the credits that were merely available.

For a detailed walkthrough with examples for the Amex Platinum, Chase Sapphire Reserve, Amex Gold, and Capital One Venture X, see How to Calculate Your Effective Annual Fee.

Quick benchmarks:

| Effective Fee | Signal |

|---|---|

| Negative | Card is paying you. Almost always worth keeping. |

| $0–$100 | Likely worth keeping if you use non-credit benefits. |

| $100–$300 | Needs closer analysis. |

| $300+ | Strong cancel candidate unless specific benefits are critical. |

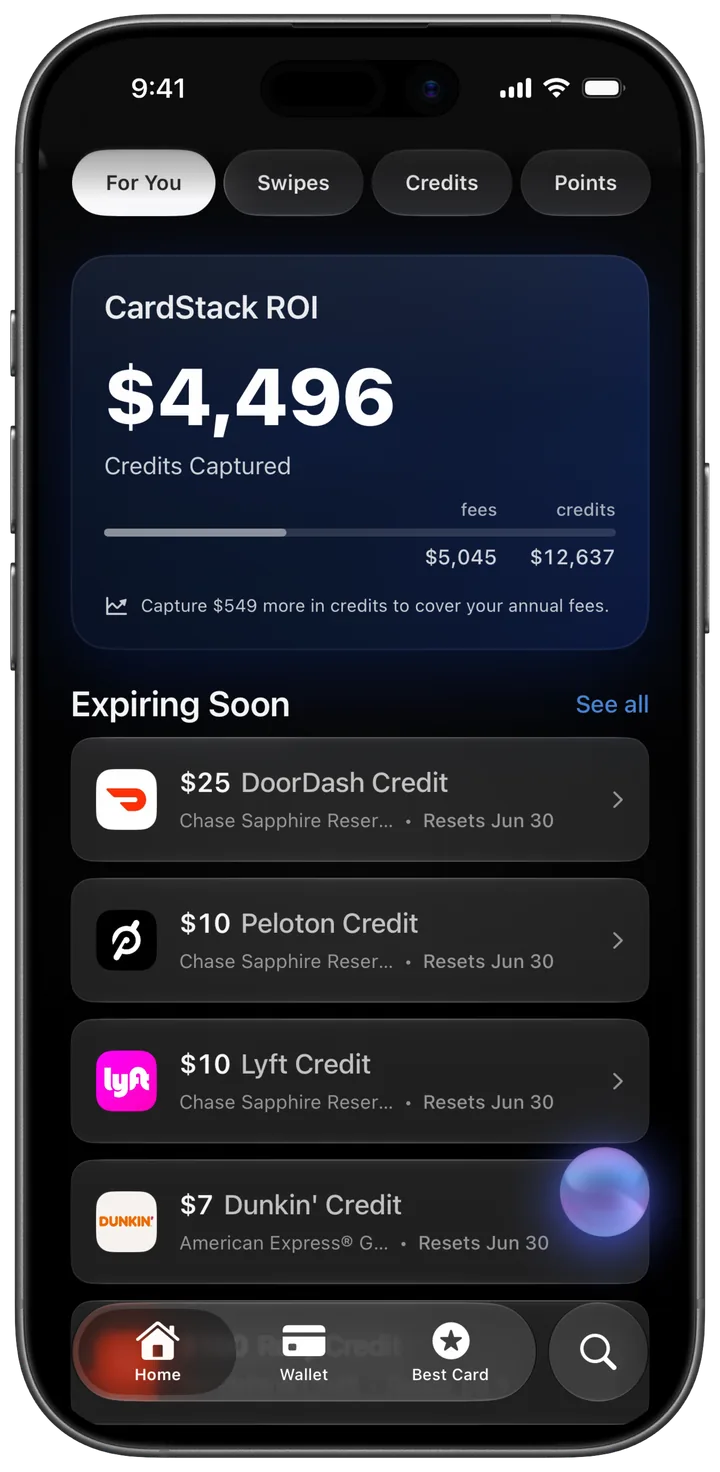

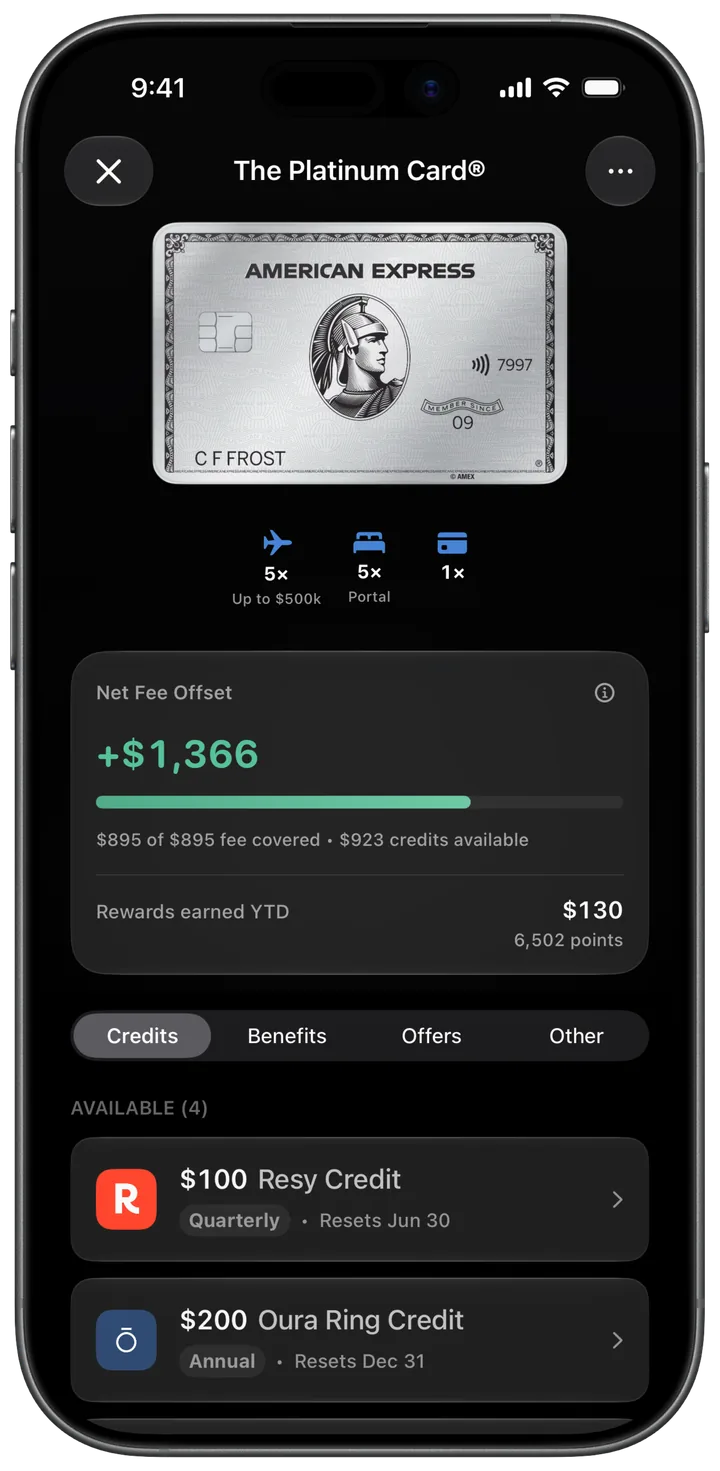

CardStack calculates your effective annual fee automatically through its Annual Verdict feature, so you do not have to dig through statements. It shows exactly which credits you used, which you missed, and what your real cost was over the past card year.

Step 2: Value the Non-Credit Benefits

Credits are easy to quantify. The rest of the card’s benefits are harder but still important.

Go through this checklist and assign a realistic dollar value to each benefit you actually used in the past year:

Travel Benefits

- Airport lounge access: How many times did you visit? What would you have spent on food/drinks otherwise? ($20–$50 per visit is a reasonable estimate.)

- Hotel status (Gold, Platinum, etc.): Did you receive upgrades, late checkout, or free breakfast? What were those worth?

- Airline status or perks: Free checked bags, priority boarding, companion tickets?

- Global Entry / TSA PreCheck credit: Worth $100 if you applied during this card year, $0 otherwise (it is every 4–5 years).

- Travel insurance: Trip delay, cancellation, lost luggage coverage. Did you file a claim? Even if you did not, do you value the coverage?

Everyday Benefits

- Purchase protection and extended warranty: Did you use it? How much was covered?

- Cell phone insurance: Some cards cover damage/theft if you pay your phone bill with the card.

- Rental car insurance: Did you decline the rental counter’s coverage because your card covers it?

- Return protection: Were you able to return something the retailer would not take back?

Earning Rate Premium

- How many points did you earn on this card that you would not have earned on a no-fee alternative?

- What is the incremental value of those points? (e.g., if you earned 4x on dining instead of 1.5x on a no-fee card, the extra 2.5x has real value)

Add up the realistic values. Lounge access you used once is worth about $30, not the “$500 in lounge access” from the issuer’s marketing page.

Step 3: Call for a Retention Offer

Before you cancel any card with an annual fee, call the issuer and ask about retention offers. Retention offers are standard practice; issuers budget for them and expect the call.

How to do it:

- Call the number on the back of your card

- Say you are considering canceling because of the annual fee

- Ask if there are any offers available to keep you as a cardholder

- Listen to the offer. Do not accept or decline on the spot. Ask for time to think about it.

Common retention offers:

- Statement credit: $100–$300 credited to your account. This directly reduces your effective fee.

- Bonus points: 10,000–50,000 points for keeping the card. Value depends on how you redeem.

- Reduced fee: Some issuers will waive part of the annual fee for one year.

- Spending bonus: “Earn 10,000 extra points if you spend $3,000 in the next 3 months.”

Retention offers vary by issuer, card, spending history, and tenure. Amex and Chase both regularly offer retention bonuses. You are more likely to receive a strong offer if you have been a long-term cardholder with significant spending.

Factor the retention offer into your math. If your effective fee is $200 and the issuer offers $150 in statement credit, your effective fee drops to $50. That might change the decision.

Step 4: Check Downstream Impacts

Canceling a card is not just about the annual fee. There are knock-on effects that can cost you money in less obvious ways.

Credit Score Impact

- Credit utilization: Closing a card reduces your total available credit, which can increase your utilization ratio and lower your score. This matters most if you carry balances on other cards.

- Average age of accounts: Closing an older card can reduce your average account age. However, closed accounts stay on your credit report for 10 years, so the impact is delayed.

- Inquiries: If you are planning to apply for a mortgage or car loan soon, avoid closing cards right before. The utilization change could cost you a better rate.

Points and Miles

- Do your points expire if you cancel? With Amex Membership Rewards, your points survive as long as you hold at least one MR-earning card (the no-fee Amex Everyday or Blue Business Plus will keep your points alive). With Chase Ultimate Rewards, you need at least one Sapphire, Freedom, or Ink card to keep the points transferable.

- Transfer partner access: If you cancel your only premium card in a program, you may lose the ability to transfer points to airline and hotel partners.

- Points devaluation: Consider whether you have unredeemed points that lose value or transferability if you close the account.

Perks You Might Not Realize You Use

- Hotel status linked to the card (Hilton Gold, Marriott Gold from Amex Platinum)

- Streaming credits that auto-renew monthly

- Uber Cash that loads automatically

- A TSA PreCheck credit that comes due next year

Review the full benefit list one more time before deciding. It is easy to forget about benefits that run on autopilot.

Step 5: Compare Alternatives

Before canceling, check whether a downgrade makes more sense. Many issuers let you product-change to a no-fee or lower-fee version of the same card, preserving your credit line and account history.

Common downgrades:

| From | To | Fee Change |

|---|---|---|

| Chase Sapphire Reserve ($795) | Chase Sapphire Preferred ($95) | Save $700 |

| Chase Sapphire Reserve ($795) | Chase Freedom Unlimited ($0) | Save $795 |

| Chase Sapphire Preferred ($95) | Chase Freedom Unlimited ($0) | Save $95 |

| Citi Strata Premier ($95) | Citi Double Cash ($0) | Save $95 |

Amex is more limited. You generally cannot downgrade a charge card (Platinum, Gold) to a credit card. You can cancel and apply for a different Amex card, but that is a new application, not a product change.

Also compare alternative cards. If you are canceling a $795 card because you are not using the travel credit, would a $395 card with a more flexible credit work better? Or would a no-fee card with a flat 2% cash back serve you just as well?

Step 6: Make the Decision

You now have four numbers:

- Effective annual fee (fee minus credits used)

- Value of non-credit benefits (lounges, insurance, earn rate premium)

- Retention offer (if any)

- Downstream cost of canceling (credit score impact, lost perks, points access)

The math:

Net cost of keeping = Effective fee − Retention offer − Value of non-credit benefits

Net cost of canceling = Downstream impacts (credit score, lost points access, lost perks)

When to definitely keep

- Your effective fee is negative or near zero

- You received a strong retention offer

- You actively use non-credit benefits (lounges, status, insurance)

- You hold significant points in the program and this is your only premium card

- You have a mortgage application coming and cannot afford a utilization spike

When to definitely cancel (or downgrade)

- Your effective fee is $300+ and you received no retention offer

- You have not used a lounge, filed an insurance claim, or redeemed the travel credit in the past year

- You have another card in the same ecosystem to preserve your points

- The card duplicates benefits you get from another card (e.g., two Priority Pass memberships)

- Your spending patterns have shifted and the card’s earn rates no longer match

When it is a close call

If the math is ambiguous, keep the card for one more year with intentionality. Set a reminder to re-evaluate in 11 months. Use the credits you have been leaving on the table. Track your benefit usage. If next year’s numbers still do not work, cancel then.

The Annual Checklist

Use this every year, one month before your annual fee posts:

- Pull credit data: What credits did I use? What did I miss?

- Calculate effective fee: Fee − credits used = my real cost

- List benefits used: Lounges, insurance, status, earn rates

- Call for retention: What offer is available?

- Check points status: Will I lose points or transfer access?

- Compare alternatives: Is there a better card for my current spending?

- Decide: Keep, downgrade, or cancel

Let CardStack Do This for You

Running through this framework manually once a year is manageable. Running it for three, four, or five premium cards gets tedious.

CardStack helps track credit usage across your cards so you can review actual value captured before making a renewal decision. Its Annual Verdict summarizes the information you have recorded; always confirm fee timing and cancellation or downgrade options with the card issuer.

The best time to evaluate a card is a month before the fee posts. The worst time is after you have already been charged and have to decide in the 30-day refund window. A system that reminds you proactively is worth having.

Final Thought

The keep-or-cancel decision is not about whether a card has good benefits. Every premium card has good benefits. The question is whether you are using enough of them to justify your fee.

An Amex Platinum that sits in a drawer earning 1x on occasional purchases while credits go unused is a $895 loss. The same card in the hands of someone who flies quarterly, dines out weekly, and tracks every credit is effectively free.

Same card. Entirely different math. Run your own numbers.

Get $1000+ a year back from your premium cards.

CardStack tracks every credit, offer, and renewal across your wallet so unused perks do not slip past their reset dates.

CardStack Insiders

Newsletter

Card news, standout deals, and product updates—straight to your inbox.

By signing up, you agree to ourTermsandPrivacy Policy. Unsubscribe anytime.

Read Next

Related articles